Most people recognize that it will be hard to make ends meet, or at least live their desired retirement lifestyles, on Social Security benefits alone. At the same time, few of us have any insights as to how long we will live. Did you know:

According to a study by Vanguard, as reported in U.S. News, the average 401(k) balance for those making over $100,000 per year is less than $250,000.

However, for those making between $75,000 and $100,000 per year, that average 401(k) balance drops to just over $100,000. And for those making less than $75,000 per year, the average 401(k) balance is well below $100,000.

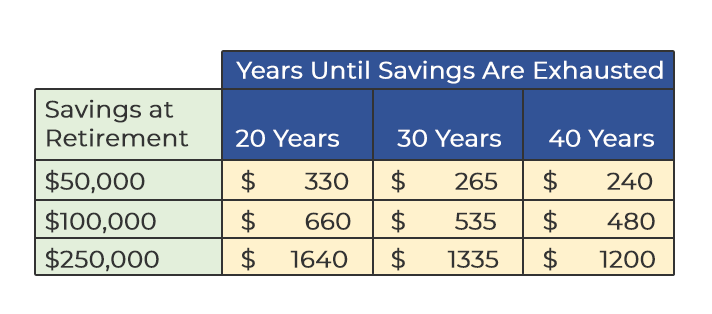

How do such balances translate to monthly income?

The yellow shaded area in the table below shows the amount of monthly income available to draw at retirement age from three account balances assuming an annual guaranteed 5% investment return:

Not surprising, the amounts above fall well short of replacing a significant portion of pre-retirement income. Also note the discrepancy in amounts available depending on if the savings are expected to last 20, 30 or 40 years. The good news is that the participants in this study have more time to grow their account balances prior to retirement.

However, the picture is further complicated by the fact that 5% annual investment returns are not guaranteed, there could be investment losses in multiple years, recessions could quickly deflate the savings balances, large medical bills will arise in retirement, inflation will reduce the purchasing power of these dollars over multiple decades, and the amounts shown above stop after the years indicated.

At ANNUA, we believe longevity risks are best managed by using a portion of retirement savings to purchase guaranteed income for life.